US Secretary of State today or tomorrow of Iran He says he will respond to the deal offer. However, if the war continues further, it will ensure stagflation. So what is this stagflation? What consequences for stocks? What are the implications for which sector? Most importantly, what does it mean for cryptocurrencies? The report prepared by the UK-based asset management company Schroders sheds light on many unknowns.

What is stagflation?

An energy shock triggered by the Iran war stagflation Concerns are increasing that it will lead to Investors are not wrong to be worried, especially with energy prices more than doubling in Europe and gasoline prices reaching their highest levels in recent years in the United States. While Asia’s access to energy was largely cut off, the closure of the Strait of Hormuz negatively affected the supply of many substances, from helium to fertilizer. So we’re talking about a war that affects everything from food to chips.

Stagflation is when real GDP growth is below the last 10-year average, of inflation (CPI) is defined as being above the 10-year average. Stagflation is generally considered the worst environment for stock markets.

Stocks

This is bad for stocks, but that’s not the point. What is important is that there are differences in sector performance in these environments, and performance differences between companies will also increase.

“There is a view that the sector spread of European stock markets may benefit them compared to the US. Given that the US dominates the global market, this could pose a problem for many investors. Alongside the oft-cited valuation argument, this is one more reason why we believe investors should avoid passive investment approaches to global equities today.”

Low growth is something that reduces sales as businesses and consumers tighten their belts. In other words, it also feeds unemployment. Demand is weak and high inflation further exacerbates this problem. In a vibrant economy, companies can pass on increased input costs to consumers. This is not so easy when demand is already weak. Instead, companies’ profit margins often take a hit, putting additional downward pressure on earnings.

The ability of central banks to stimulate demand through interest rate cuts is also restricted, as well as the weakening of companies’ fundamental indicators. When inflation is high, central banks often want to raise interest rates, not lower them, to control inflation. And higher interest rates risk making the “recession” worse. However, if they reduce interest rates, this poses a risk of pushing inflation even higher. There is no easy option.

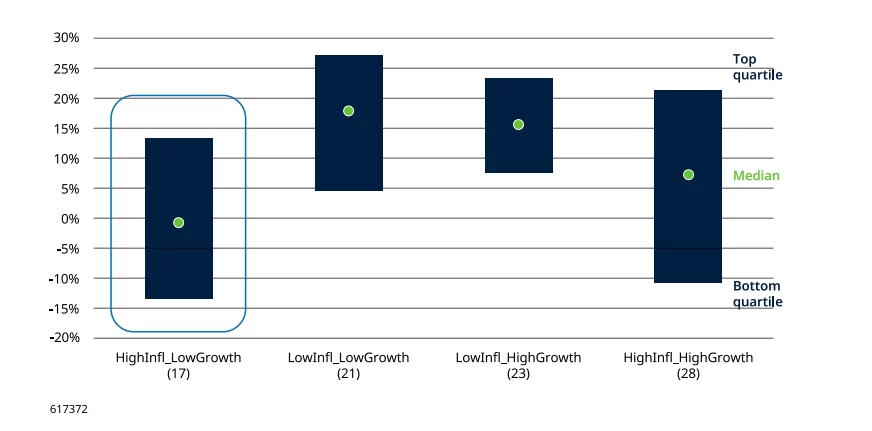

Based on data since 1926, the annual median real return during stagflation years has been approximately 0%. This is less than what investors typically expect from stocks over the long term, but earning near-inflation returns in a high-inflation environment isn’t a bad outcome.

Analysts say that in about half of these periods, stocks performed like the best of the worst. Half of all results fell within the blue shaded area, a quarter were above and a quarter were below this area.

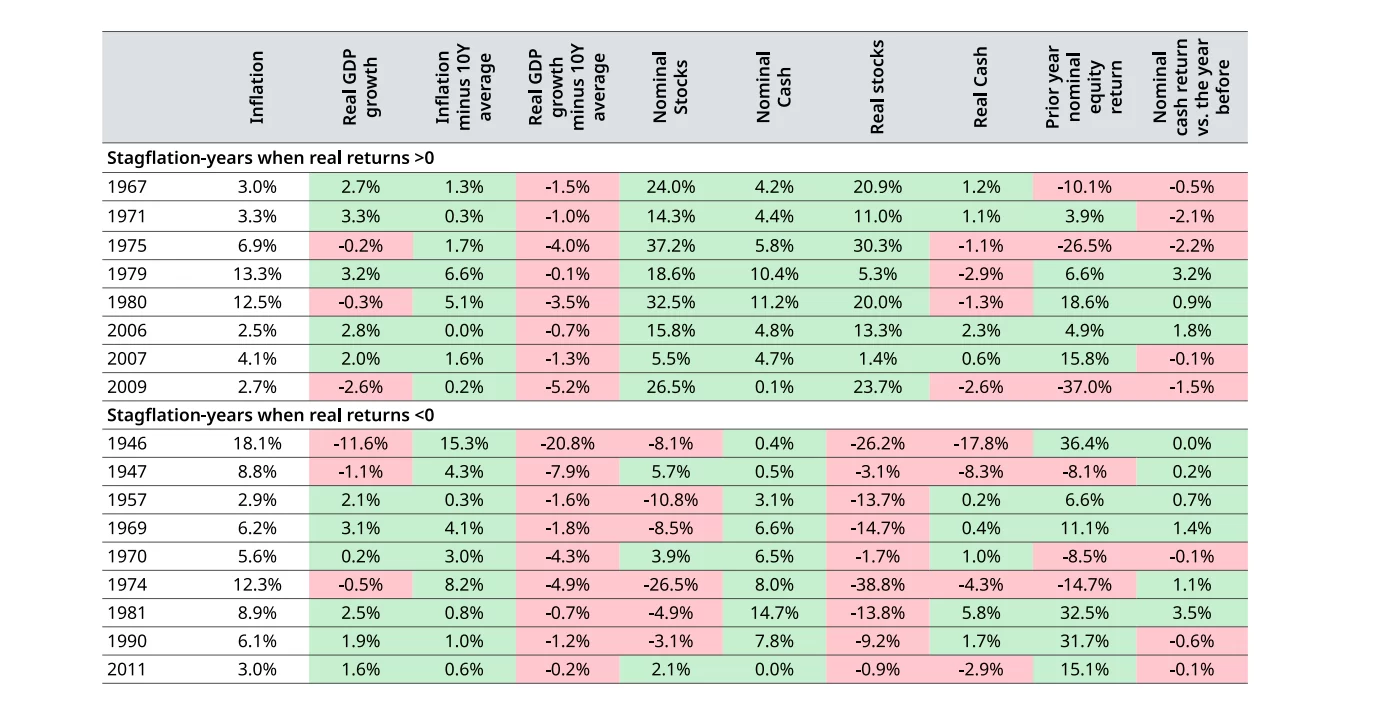

The number of stagflation years with positive real returns is quite small, with only eight (1967, 1971, 1975, 1979, 1980, 2006, 2007, 2009); Therefore, you need to think carefully when taking bold steps in these periods.

Positive (and negative) real returns during stagflation do not depend on the previous year’s market performance or interest rate cuts.

Sector Based

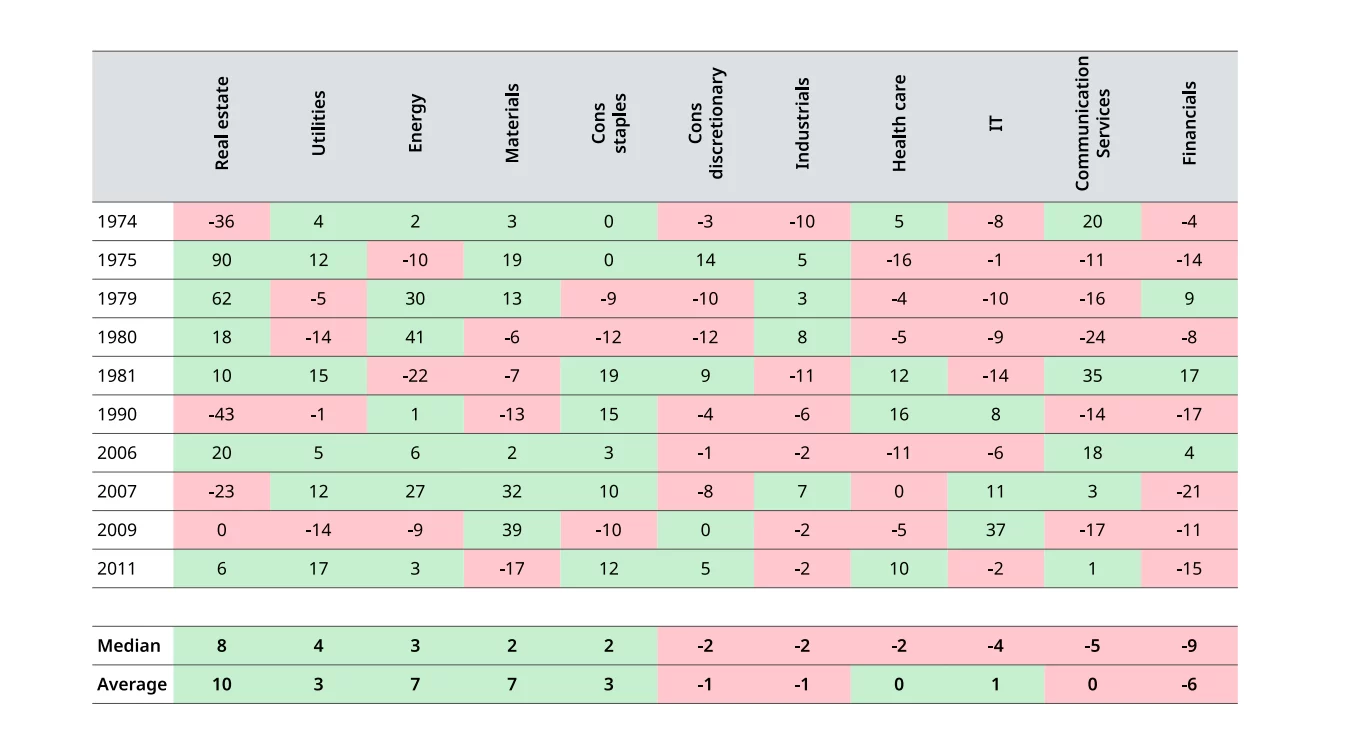

So which sectors are performing how? Sectoral data can be monitored since 1974. This makes it difficult to understand the sectoral impact of all stagflation periods. Moreover, since sector representatives change periodically, we need to look at this more carefully. While communications services used to consist of telecom companies like AT&T, today Alphabet (Google) and Meta account for almost three-quarters of the industry by market cap (as of February 28, 2026). Therefore, less confidence should be placed in conclusions drawn from historical analysis.

Sectoral performance is as above.

“Defensive sectors such as utilities and consumer staples perform relatively well because demand is less sensitive to the economic cycle. Energy and raw materials companies have generally performed well because high commodity prices were a cause of high inflation during stagflation, which remains a risk now.”

The healthcare sector is also generally classified as a defensive sector (its performance is less volatile on average than the performance of the general market), so it is interesting that its performance fell short of expectations during the 1974-2025 period when growth was low and inflation was high.

So-called “real assets” such as real estate may perform relatively well, but this sector is also one of the sectors with the widest range of results. In the case of individual investments, performance depends on the sector of the real estate market, the length of the lease and whether it is subject to inflation, debt maturity profile and other factors. If we enter stagflation, real estate investors must understand the operational risk of their tenants. Discretionary consumer goods often underperform staple consumer goods as individuals cut back on unnecessary spending.

IT and communications services also have a poor track record. This is due to a combination of rising supply costs and demand weakness, but also valuation effects. “IT companies, especially growth-oriented ones, often have high price-to-earnings (P/E) ratios as investors expect strong future earnings.”

Cryptocurrencies and Stagflation

The US market is considered risky due to its high weighting to the technology sector, which is struggling with stagflation. of the USA in stagflation index in this process since its total allocation to well-performing sectors is only 15%. to crypto The damage is likely to increase.

Japan is at a disadvantage due to its 44% dependence on global trade-sensitive industrial and luxury consumer goods. Combined with the damage caused by this war to the energy flow to Asia (in case the war is prolonged), carry trade discussions may again occupy our agenda in a stagflation environment. this too of cryptocurrencies It is against.

Although Bitcoin seems to have diverged positively in the war environment for a short time, we have to accept that it is in the balancing phase with the “realization” of a development that is overpriced. Bitcoin neither protects against inflation nor provides an escape amid the anxiety of war. Although the contradiction in its performance before and during the risks forces some to make exaggerated comments, for now (Bitcoin) has not proven itself in this regard.

The idea that stagflation automatically means a market crash is not based on historical data. However, we must say that the possible scenario in which the Fed’s delayed interest rate cuts will coincide with interest rate increases in Europe is not that unlikely. This will be challenging for the US and risk markets.