Today, the AK Party presented an important bill regarding cryptocurrencies with the signature of 48 members of parliament. We shared a summary of the important details that first attracted attention at the last minute, but now we will discuss all the items. This is the most important tax step we have seen so far in Türkiye regarding cryptocurrencies.

Justification of the Bill

In the justification section it is clearly stated that “tax The motivation for “covering areas outside the scope of cryptocurrencies The taxation phase, which has been awaited for a long time but which investors are uncomfortable with, is starting for Türkiye as well.

Aksaray MV Hüseyin ALTINSOY and Elazığ MV Ejder AÇIKKAPI are the first signatories of the bill. There are many details in the bill, from Foundation Universities to betting advertisements, so it is not a bill specific to cryptocurrency. The law amendment proposal was delivered to a total of 4 commissions today, including the Planning and Budget Commission. After the work here, a vote will be taken.

Tax on Cryptocurrencies

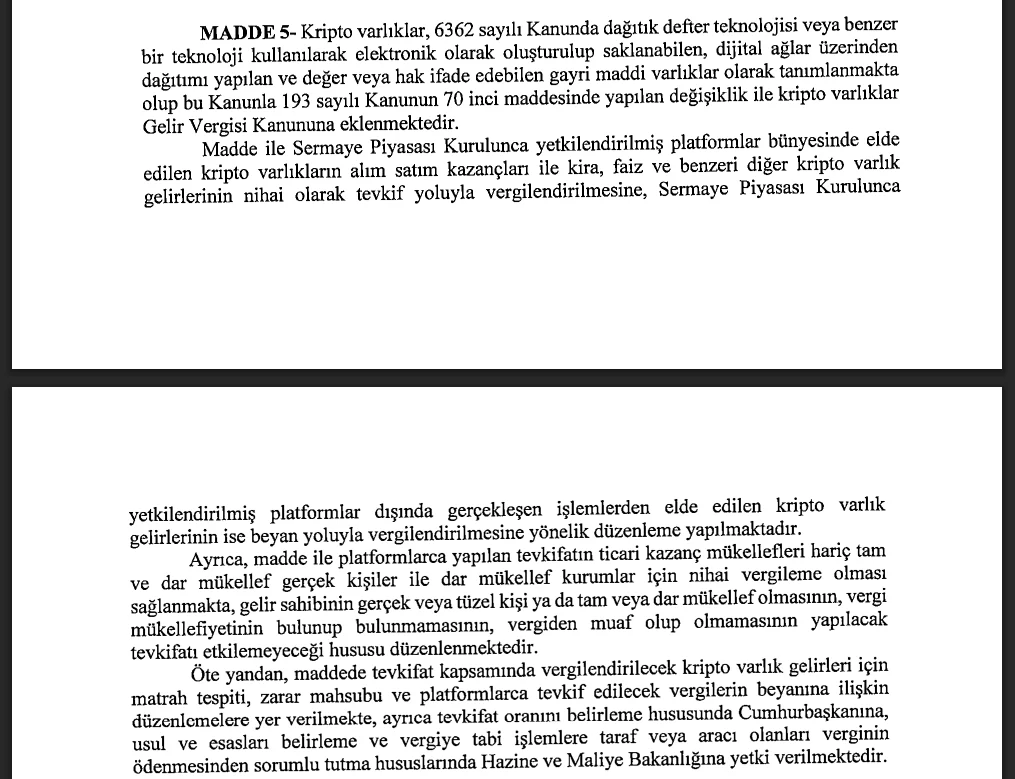

Income Tax Law Crypto assets will be added to Article 70, so that income derived from crypto can be taxed.

“The article regulates the final taxation of crypto asset trading gains and rent, interest and other similar crypto asset income obtained within the platforms authorized by the Capital Markets Board, through withholding. The crypto asset income obtained from transactions realized outside the platforms authorized by the Capital Markets Board will be taxed through declaration.

In addition, the article ensures that the withholdings made by the platforms are final taxation for full and limited taxpayer real persons and limited taxpayer institutions, excluding commercial income taxpayers, and it is regulated that whether the income owner is a real or legal person, full or limited taxpayer, whether he or she is tax liable, whether he or she is exempt from tax will not affect the withholding.” – Bill of Law

Gains arising from the disposal of crypto assets will be included in the scope of capital gains. Also included in commercial enterprise crypto assets The necessary phrase is also added to the article of law so that the gains arising from the disposal are considered as commercial income.

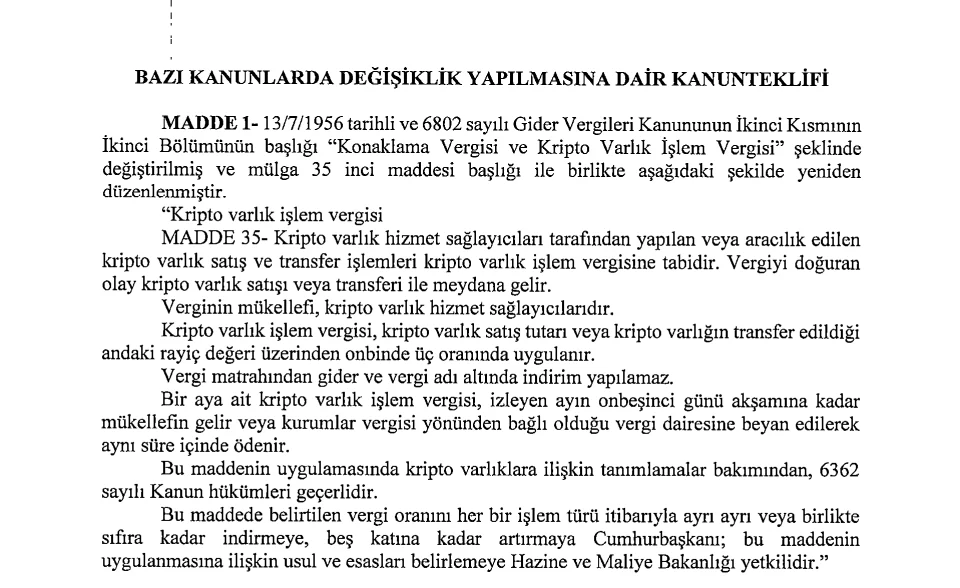

In order to collect tax on cryptocurrencies, the title of the Second Part of the Second Part of the Expense Taxes Law No. 6802 dated 13/7/1956 will be changed to “Accommodation Tax and Crypto Asset Transaction Tax”. According to this article, crypto asset sales and transfer transactions made or mediated by crypto asset service providers will be subject to crypto asset transaction tax.

- The taxpayer will be the crypto asset service providers.

- Crypto-asset transaction tax will be applied at a rate of three ten thousandths of the crypto-asset sales amount or the current value of the crypto-asset at the time it is transferred.

- No deductions can be made from the tax base under the name of expenses and taxes.

- Crypto asset transaction tax for a month will be declared to the tax office to which the taxpayer is affiliated in terms of income or corporate tax by the evening of the fifteenth day of the following month and paid within the same period.

Income obtained from crypto asset transactions carried out outside the platforms subject to Law No. 6362 will be declared with the annual income tax return. Losses arising from crypto asset transactions can only be offset against the profits derived from these assets. Cryptocurrency exchanges It will deduct 10% tax from earnings from crypto transactions every 3 months.

So, we face 2 taxes.

- Purchase, sale and transfer tax at the rate of 3 per ten thousand. This is a very small number.

- 10% earnings tax to be collected from earnings every 3 months.

Loss offset is only possible within the calendar year, and the 10% figure is much more than expected. That’s why cryptocurrency investors in Türkiye will not be happy with the situation.

When will it become law?

Cryptoasset transaction tax and the articles regarding the 10% withholding tax (earnings tax) (Articles 1, 3, 4, 5) will come into force at the beginning of the second month after the law is published. The proposal will first be discussed in the Planning and Budget Commission (Main Commission) and the secondary commissions, where the articles will be given their final form. There may be an improvement regarding the 10% tax in this process, but since it is a package arrangement, it does not seem like much time will be spent on crypto.

The text passed by the commission comes to the General Assembly of the Turkish Grand National Assembly. First the whole thing is voted on, then the articles are voted on one by one. Then the President signs it within 15 days and has it published in the Official Gazette. The law is likely to become law in Spring or Summer 2026. If published in March or April, crypto taxes It will not be until June or July 2026 (due to the second menstrual rule) that it will begin to be implemented.

So, will there be taxation for transactions before it becomes law? Article 18 of the proposal clearly states that the tax will start “at the beginning of the second month following its publication”. This means that your earnings before the law was enacted will not be subject to this law. “Non-retroactivity” is essential in tax law. A new tax regulation can only be applied to events and transactions after its entry into force. Since there is no crypto tax obligation for individual investors within the framework of current laws as of 2026, the earnings earned until this law is enacted will be seen within the scope of the current exemption. As we mentioned in the introduction, the purpose of the work is expressed as “taxing untaxed areas”.